Commercial Real Estate Due Diligence Checklist: What to Verify Before Closing

Due diligence is where deals survive or die. The offering memorandum tells you what the seller wants you to believe. Due diligence tells you what’s actually true.

Every week, experienced investors walk away from deals during due diligence — not because the property is bad, but because the numbers don’t match the story. The rent roll has a tenant in default. The roof needs $400K in repairs. The property taxes will double on reassessment.

This guide provides a comprehensive due diligence checklist organized by category, with practical guidance on what to look for and what should trigger a deeper investigation or price renegotiation.

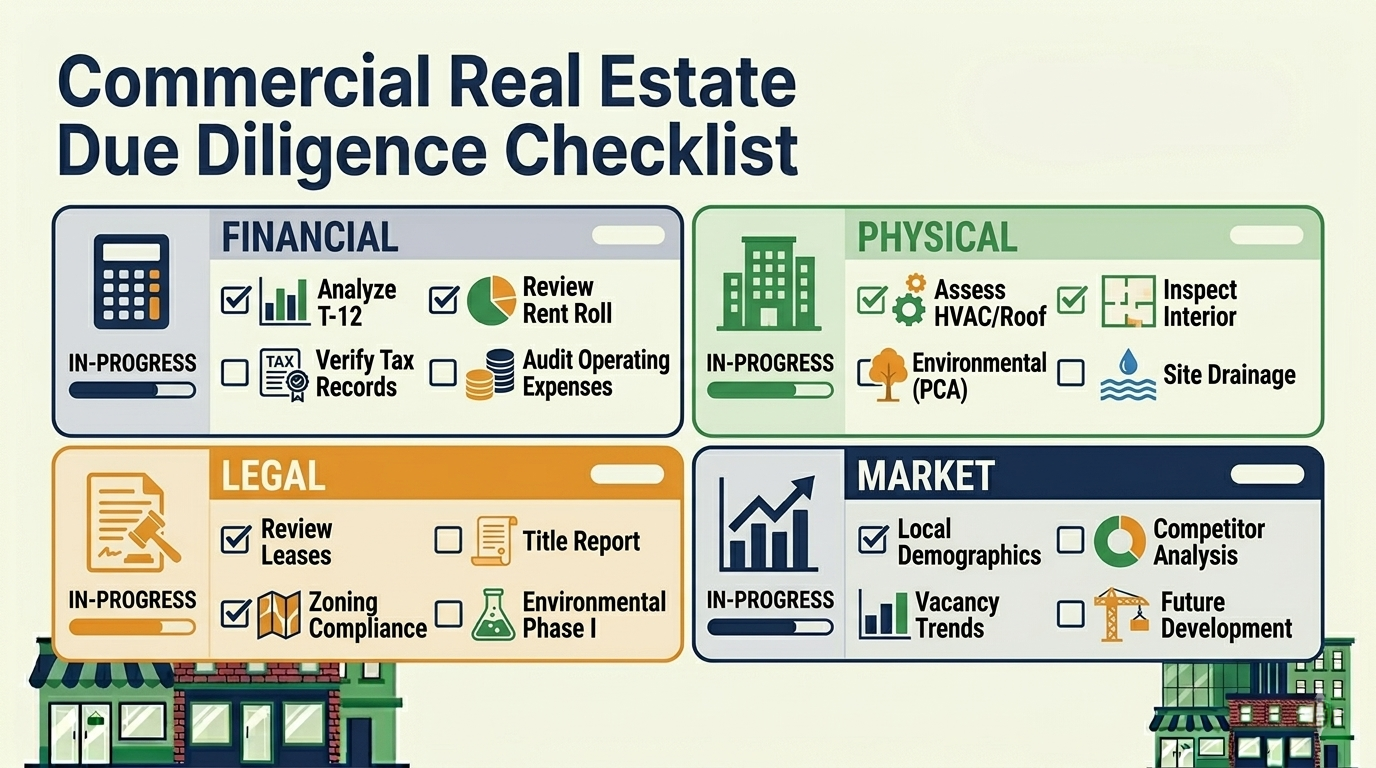

Financial Due Diligence

Income Verification

- T-12 operating statement (trailing twelve months, month-by-month)

- T-3 operating statements (three years of annual financials for trend analysis)

- Rent roll (current, within 30 days of LOI)

- Lease abstracts for all tenants (full lease docs for top 5 tenants by revenue)

- Accounts receivable aging report (who owes what, and for how long)

- Security deposit register (amounts held, any applied or refunded)

- Other income documentation (parking, storage, antenna leases, vending contracts)

- Historical occupancy report (5 years if available)

What to verify:

- Does T-12 revenue match the rent roll? Cross-reference total annual rent against the sum of all tenant obligations.

- Are there tenants paying below rent roll rates? Check for concessions, abatements, or workout agreements not reflected in the rent roll.

- Is the AR aging report clean? Tenants 60+ days past due represent real collection risk.

Expense Verification

- Property tax bills (current year plus 2 years prior)

- Insurance declarations page (current policy, not just premium amount)

- Utility bills (12 months of actuals from each provider)

- Service contracts (HVAC, elevator, janitorial, landscaping, security, pest control)

- Management agreement (fee structure, termination provisions)

- Capital expenditure history (3-5 years of CapEx spending)

What to verify:

- Will property taxes be reassessed on sale? Contact the county assessor’s office. In reassessment states, this is often the single largest post-acquisition expense increase.

- Are any service contracts above market rate or long-term? You may inherit unfavorable agreements.

- What has the seller spent on CapEx vs. what should they have spent? Deferred maintenance shows up as artificially low R&M. This is especially critical for value-add acquisitions where renovation budgets hinge on accurate condition assessment.

Debt and Encumbrances

- Existing loan documents (note, deed of trust, guaranty, loan agreement) — see our CRE loan types guide for terminology

- Loan balance and payoff amount (current principal balance + prepayment penalty)

- Assumption terms (if assuming existing debt — rate, remaining term, conditions)

- UCC filings (liens on personal property or fixtures)

- Tax lien search (unpaid property taxes, IRS liens)

- Subordination/non-disturbance agreements (SNDAs) for key tenants

Physical Due Diligence

Property Condition Assessment (PCA)

- Roof inspection (type, age, remaining useful life, leak history)

- HVAC inspection (age of each unit, maintenance records, replacement timeline)

- Electrical systems (panel capacity, code compliance, upgrade needs)

- Plumbing (pipe material, water pressure, sewage/drainage issues)

- Building envelope (exterior walls, windows, insulation, water infiltration)

- Parking lot/structure (surface condition, striping, lighting, drainage)

- Elevator inspection (certification current, maintenance history, modernization needs)

- Fire/life safety (sprinkler system, fire alarms, emergency lighting, ADA compliance)

Critical numbers:

| System | Typical Useful Life | Replacement Cost Estimate |

|---|---|---|

| Roof (flat/commercial) | 20-25 years | $6-12/SF |

| HVAC (rooftop units) | 15-20 years | $3,000-8,000/ton |

| Parking lot (asphalt) | 15-20 years | $3-6/SF |

| Elevator modernization | 25-30 years | $100K-300K per cab |

If the property condition assessment reveals $500K in deferred CapEx, that needs to be credited against the purchase price or escrowed at closing. Don’t fund it from future cash flow — it’s the seller’s deferred liability.

Environmental

- Phase I Environmental Site Assessment (ESA) — baseline report identifying potential contamination. Required by most lenders.

- Phase II ESA (if Phase I identifies recognized environmental conditions) — soil/groundwater testing.

- Asbestos survey (buildings pre-1980)

- Lead paint assessment (buildings pre-1978)

- Underground storage tank records (gas stations, industrial sites)

- Flood zone certification (FEMA map, flood insurance requirements)

- Radon testing (certain regions)

Deal-killer scenarios:

- Active contamination with no responsible party (you inherit liability)

- Property in 100-year flood zone with inadequate insurance

- Asbestos in areas requiring immediate abatement (not just encapsulation)

Legal Due Diligence

Title and Survey

- Preliminary title report (identifies liens, easements, encroachments, restrictions)

- ALTA survey (boundary survey showing improvements, easements, setbacks, flood zones)

- Title insurance commitment (coverage amount, exceptions listed)

- CC&Rs and deed restrictions (use restrictions, building restrictions, HOA obligations)

- Easement agreements (utility, access, drainage — anything crossing the property)

What to verify:

- Are there any title exceptions that restrict your intended use?

- Do survey encroachments create risk? (Adjacent building overlapping property line, unapproved structures)

- Are there reciprocal easement agreements (REAs) with adjacent property owners that affect parking, access, or signage?

Lease Review

- Full executed copies of all leases

- All lease amendments, extensions, and addenda

- Tenant estoppel certificates (tenant confirms lease terms, no defaults, no claims)

- Guaranty agreements (personal or corporate guarantees on leases)

- Subleases and assignments (any tenants not the original lessee?)

- Outstanding landlord obligations (TI still owed, free rent remaining, expansion options)

Critical lease provisions to flag:

- Termination rights — Can any tenant terminate early? On what terms?

- Exclusive use clauses — Do any tenants have exclusivity that limits your ability to lease to competing businesses?

- ROFO/ROFR — Right of first offer or first refusal on adjacent space?

- Purchase options — Does any tenant have the right to buy the property?

- Expense caps — Are any tenant recoveries capped, limiting your ability to pass through rising expenses?

Zoning and Entitlements

- Zoning verification letter (current zoning, permitted uses, variances)

- Certificate of occupancy (current and matching actual use)

- Building permits (recent work properly permitted and closed)

- ADA compliance assessment (especially for older buildings and tenant spaces)

- Parking ratio verification (actual count vs. code requirement vs. lease obligations)

Market Due Diligence

Comparable Analysis

- Comparable rental rates (competing properties, same submarket, same class)

- Comparable sale prices (recent transactions for similar property types)

- Vacancy rates (submarket and market level, for your property type)

- Absorption trends (is the submarket adding or losing tenants?)

- New construction pipeline (what’s being built that will compete for tenants?)

Why this matters for underwriting:

- If market rents are $22/SF and your rent roll averages $25/SF, you have rolldown risk — rents may decrease when leases expire.

- If the submarket has 2M SF of new office construction delivering in 18 months, vacancy rates may increase and push lease-up timelines longer.

- Comparable sales validate (or invalidate) the seller’s asking price.

Demographic and Economic

- Population and employment trends (growing or shrinking market?)

- Major employer diversification (is the market dependent on one industry?)

- Infrastructure changes (new highways, transit, development projects)

- Tax and regulatory environment (rent control, development restrictions, tax incentives)

The Due Diligence Timeline

Most purchase agreements provide 30-60 days for due diligence, though complex deals may negotiate 90 days. Here’s a realistic timeline:

| Week | Priority |

|---|---|

| Week 1 | Order title, survey, PCA, Phase I. Request all financial docs from seller. Begin lease review. |

| Week 2 | Receive and review T-12, rent roll, leases. Send estoppel certificates to tenants. |

| Week 3 | PCA and Phase I reports arrive. Evaluate CapEx needs. Normalize the T-12. |

| Week 4 | Complete financial model. Quantify any price adjustments. Meet with insurance/tax advisors. |

| Week 5-6 | Negotiate credits, reps and warranties, and closing conditions. Finalize financing. |

Don’t wait until Week 4 to order your property condition report. The most common cause of missed due diligence deadlines is late-arriving third-party reports.

When to Walk Away

Not every problem is a deal-killer, but some are:

- Environmental contamination with unclear liability or remediation cost

- Structural deficiency requiring major capital that exceeds your return threshold

- Anchor tenant exercising early termination before closing

- Title defects that can’t be cured or insured

- Seller’s financials don’t reconcile after multiple requests for clarification

Walking away after investing in due diligence costs feels expensive. Closing on a property with undiscovered problems costs far more.

Key Takeaways

-

Start third-party reports immediately. PCA, Phase I, title, and survey have the longest lead times and the highest deal-breaking potential.

-

Cross-reference everything. The rent roll against the T-12, the T-12 against bank statements, the leases against the rent roll. Discrepancies are where problems hide.

-

Normalize for your ownership. The seller’s T-12 reflects their management, not yours. Adjust taxes, management fees, R&M, and insurance to your reality.

-

Quantify every issue in dollars. A leaking roof isn’t a “concern” — it’s a $180,000 credit against the purchase price. Take emotions out of negotiations.

-

Your due diligence informs your proforma. Every assumption in your financial model should trace back to something you verified during this process.

Eric Davis is the founder of Nordic Real Estate Services and creator of Solsten, a CRE analysis platform that turns your due diligence findings into a living proforma with automated projections, risk scoring, and scenario analysis. Start your analysis free →

Try Solsten Free

See everything we discussed in action — no credit card required.

Start Your Free AnalysisRelated Articles

Load-Bearing Math: Where AI Belongs in CRE — and Where It Doesn't

AI is transforming how CRE professionals research, draft, and summarize. But underwriting, debt sizing, waterfall distributions, and LP reporting need engineered software — not generated paragraphs. Here's why.

How to Calculate Operating Expenses for Commercial Real Estate

A complete guide to CRE operating expenses — categories, fixed vs. variable, below-the-line items, and how expense modeling affects your NOI, DSCR, and investment returns.

What Is Effective Gross Income (EGI) in Commercial Real Estate?

Understand Effective Gross Income (EGI) in CRE — how it's calculated, why it matters more than PGI, and how vacancy, credit loss, and other income affect your underwriting.