Commercial Real Estate Loan Types: A Complete Guide to CRE Financing

The financing structure on a commercial real estate deal affects every return metric you calculate. The same property can produce a 12% levered IRR with one loan structure and an 18% IRR with another — or a negative return if the debt is wrong.

Understanding CRE loan types isn’t just a financing exercise. It’s an underwriting exercise. The terms, maturity, amortization, and covenants on your debt directly drive your cash-on-cash return, your exit flexibility, and your downside risk.

This guide covers the major CRE loan types, when each makes sense, the key terms to negotiate, and how financing decisions flow into your proforma.

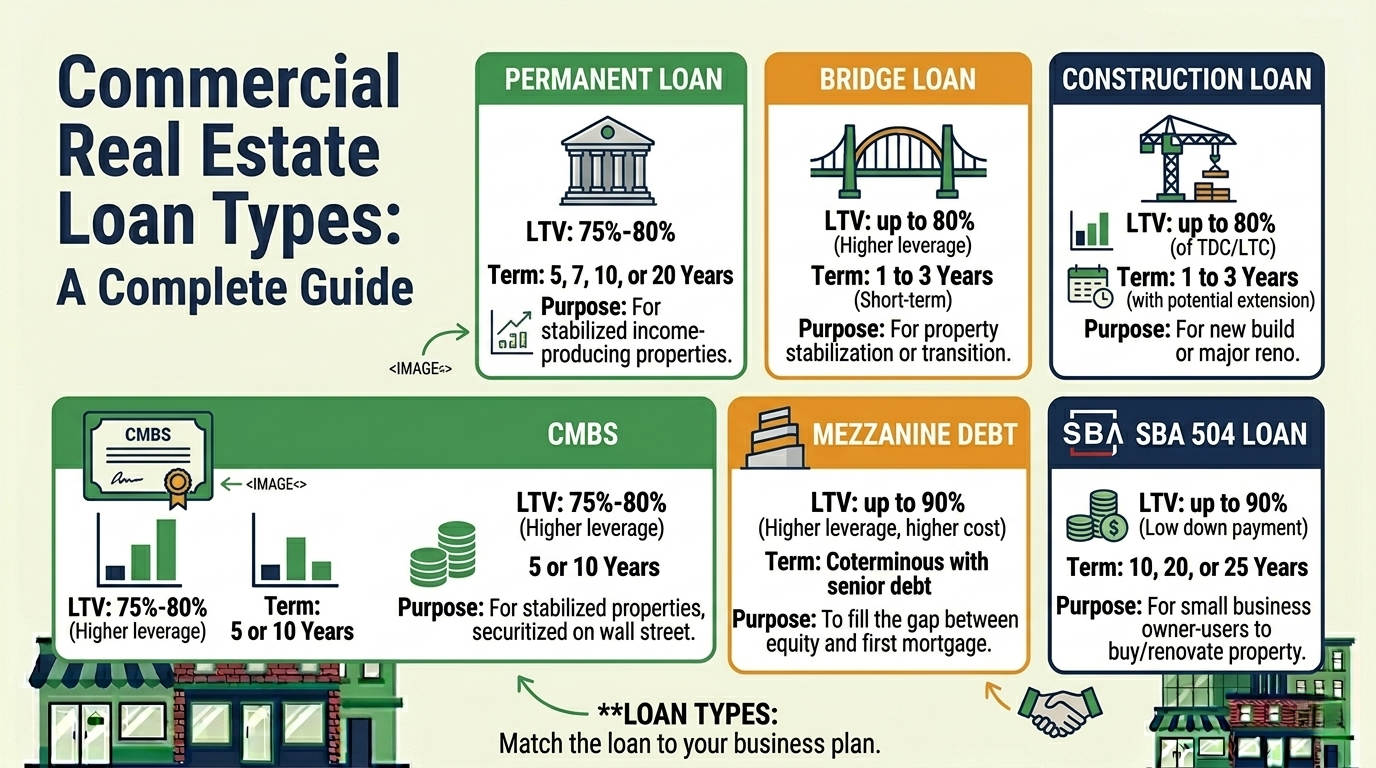

Permanent Loans (Conventional)

The most common CRE financing structure. A permanent loan is a long-term mortgage on a stabilized, income-producing property.

Typical Terms:

| Parameter | Range |

|---|---|

| Loan-to-Value (LTV) | 60 – 75% |

| Interest Rate | 5.5 – 7.5% (market dependent) |

| Term | 5 – 10 years |

| Amortization | 25 – 30 years |

| DSCR Requirement | 1.20x – 1.35x |

| Prepayment | Yield maintenance or defeasance |

How it works: The lender sizes the loan based on the LESSER of the LTV constraint and the DSCR constraint. Your effective leverage is usually determined by whichever metric is more restrictive.

Sizing example:

Property value: $5,000,000 — NOI: $350,000

LTV constraint (70%):

DSCR constraint (1.25x):

At 6.5% on a 25-year amortization, $280K annual debt service supports a loan of approximately $3,720,000.

The LTV constraint is binding here, so max loan = $3,500,000. The NOI used for DSCR sizing should come from your normalized T-12 — not the seller’s pro forma.

When to use: Stabilized properties with predictable cash flow, long-term holds, core and core-plus strategies.

Bridge Loans

Bridge loans provide short-term financing for properties in transition — lease-up plays, value-add renovations, or acquisitions that don’t yet qualify for permanent financing.

Typical Terms:

| Parameter | Range |

|---|---|

| LTV / LTC | 65 – 80% of cost or value |

| Interest Rate | 7 – 10% (floating, typically SOFR + spread) |

| Term | 1 – 3 years + extension options |

| Amortization | Interest-only |

| DSCR Requirement | Often none (asset-based lending) |

| Prepayment | Flexible (no yield maintenance) |

How it works: Bridge lenders underwrite to the business plan, not just current income. They typically require a detailed renovation budget, lease-up timeline, and exit strategy (refinance into permanent debt or sell).

Key considerations:

- Interest-only payments preserve cash during renovation and lease-up

- Floating rates create interest rate risk — budget for rate increases

- Extension fees (0.25-0.50% of loan balance) add up if your business plan takes longer than expected

- Exit risk — You must refinance or sell before maturity. If the property isn’t stabilized by then, you’re in a difficult position.

When to use: Value-add acquisitions, lease-up plays, properties needing renovation before qualifying for permanent financing.

Construction Loans

Construction loans finance ground-up development or major property repositioning.

Typical Terms:

| Parameter | Range |

|---|---|

| Loan-to-Cost (LTC) | 55 – 70% |

| Interest Rate | 7 – 9% (floating) |

| Term | 18 – 36 months |

| Amortization | Interest-only (on drawn balance) |

| Reserve Requirements | Interest reserve, completion guarantee |

| Draw Schedule | Progress-based draws verified by inspector |

How it works: Unlike a permanent loan where you receive the full amount at closing, construction loan funds are disbursed (“drawn”) as work is completed. You only pay interest on the amount drawn, not the full commitment.

Draw process:

- Developer completes a phase of work

- Lender sends an inspector to verify completion

- Inspector certifies the work

- Lender releases the next draw

Key risks:

- Cost overruns — If construction costs exceed the budget, the developer must fund the gap from equity. The lender won’t increase the loan.

- Completion guarantee — The developer (or GP) personally guarantees the project will be completed, even if it costs more than budgeted.

- Interest reserve — Part of the loan is set aside to cover interest payments during construction until the property generates income.

When to use: Ground-up development, major gut renovations, change-of-use conversions.

CMBS Loans (Commercial Mortgage-Backed Securities)

CMBS loans are originated by lenders, then packaged and sold to bond investors in securitized pools. The loan is serviced by a third-party special servicer, not the original lender.

Typical Terms:

| Parameter | Range |

|---|---|

| LTV | 65 – 75% |

| Interest Rate | Competitive (often lower than bank) |

| Term | 10 years (most common) |

| Amortization | 25 – 30 years |

| DSCR Requirement | 1.25x+ |

| Prepayment | Defeasance or yield maintenance |

| Lockout Period | 2-5 years (no prepayment allowed) |

Advantages:

- Lower interest rates (capital markets pricing)

- Non-recourse — no personal guarantee from the borrower

- Higher leverage than some bank loans

Disadvantages:

- Extremely rigid — modifications, lease approvals, and property changes require special servicer consent

- Prepayment is expensive and complex

- Reporting requirements are extensive

- The servicer’s incentives may not align with the borrower’s

When to use: Long-term holds on stabilized properties where you don’t anticipate needing flexibility. Best for low-touch assets with predictable cash flow.

Mezzanine Debt

Mezzanine (“mezz”) debt fills the gap between the senior loan and equity. It’s subordinate to the first mortgage but senior to equity.

Typical Terms:

| Parameter | Range |

|---|---|

| Position | Between 65% LTV (senior) and 80-85% total leverage |

| Interest Rate | 10 – 15% |

| Term | Matches or is shorter than senior loan |

| Security | Pledge of ownership interest (not a lien on property) |

| Intercreditor | Requires intercreditor agreement with senior lender |

Example capital stack:

| Layer | Amount | % of Value | Cost |

|---|---|---|---|

| Senior Loan | $3,500,000 | 70% | 6.5% |

| Mezzanine | $750,000 | 15% | 12.0% |

| Equity | $750,000 | 15% | Target 18% IRR |

| Total | $5,000,000 | 100% |

Mezzanine debt increases leverage (and therefore levered returns) but also increases risk. If NOI drops, the senior debt service must be paid first, then the mezzanine, leaving less cash for equity holders. In practice, mezzanine debt often resembles preferred equity — the distinction depends on the legal structure and waterfall position.

When to use: When you need higher leverage than the senior loan provides and want to limit equity dilution. Common in value-add and development deals where equity investors want higher returns.

SBA 504 Loans

The SBA 504 program provides favorable financing for owner-occupied commercial properties.

Typical Terms:

| Parameter | Terms |

|---|---|

| Structure | Bank first mortgage (50%) + CDC note (40%) + Borrower equity (10%) |

| Interest Rate | Below market (CDC note is fixed, tied to Treasury rates) |

| Term | 20-25 years fixed (CDC note) |

| Amortization | Fully amortizing |

| Minimum Occupancy | 51% owner-occupied |

| Max Loan | $5.5M CDC portion (up to $16.5M for energy projects) |

Advantages:

- Only 10% equity required (vs. 25-30% for conventional)

- Very long fixed-rate terms

- Below-market interest rate on CDC portion

- Fully amortizing (building equity faster)

Disadvantages:

- Must be owner-occupied (51%+ of space)

- Lengthy approval process (60-90 days)

- Multiple closing costs (two loans, CDC fees)

- Personal guarantee required

When to use: Small business owners purchasing property for their operations. The 10% equity requirement and below-market rates make SBA 504 one of the best financing tools available — if you qualify.

How Financing Affects Your Proforma

Every loan structure decision flows directly into your financial model:

Amortization period affects annual debt service:

Where $r$ = monthly interest rate and $n$ = total number of payments.

A $3.5M loan at 6.5% with 25-year amortization requires $287,000/year in debt service. The same loan with 30-year amortization requires $266,000/year — a $21K annual cash flow difference.

Interest-only periods boost early cash flow but defer principal paydown. When you refinance or sell, you still owe the full original balance.

Floating rate exposure means your debt service changes with market rates. A 200 basis point rate increase on a $3.5M floating rate loan adds $70,000/year in interest cost.

Prepayment structure determines your exit flexibility. Yield maintenance can cost 5-15% of the loan balance in the early years — destroying your IRR if you sell ahead of schedule.

Key Takeaways

-

Match the loan structure to the business plan. Bridge for transitional assets, permanent for stabilized, construction for development.

-

DSCR often constrains leverage more than LTV. Calculate both constraints and size to the more restrictive one.

-

Interest-only helps during lease-up but delays equity building. Model the full amortization schedule in your proforma to see the true impact.

-

CMBS offers the best rates but the least flexibility. Only appropriate for low-touch, long-term holds.

-

Every financing decision is an underwriting decision. Rate, leverage, term, and prepayment all flow directly into your IRR, cash-on-cash, and equity multiple.

Eric Davis is the founder of Nordic Real Estate Services and creator of Solsten, a CRE analysis platform with multi-loan modeling, construction draw tracking, amortization scheduling, and DSCR analysis built into the proforma engine. Model your financing →

Try Solsten Free

See everything we discussed in action — no credit card required.

Start Your Free AnalysisRelated Articles

Cap Rates, Do They Really Matter?

Cap rates are the most used metric in CRE — but relying on them alone is dangerous. Learn what cap rates miss and which metrics give you the full picture.

What Is Cash-On-Cash Return? Formula, Example, and Benchmark

Cash-on-cash return is annual pre-tax cash flow divided by total cash invested. This guide walks through the formula, a step-by-step CRE example, and what counts as a good benchmark.

Commercial Real Estate Due Diligence Checklist: What to Verify Before Closing

Complete CRE due diligence checklist covering financial, physical, legal, environmental, and market verification — what to request, what to analyze, and what kills deals.