Preferred Return in Real Estate: How It Works, How It's Calculated, and Why It Matters

Preferred return is the single most misunderstood term in CRE syndication. I’ve seen experienced operators argue over whether “8% pref” means simple or compound accrual — and the difference in actual dollar payouts can be enormous.

This guide breaks down exactly how preferred return works, the math behind simple vs. compound accrual, how catch-up provisions interact with the pref, and what to look for in an operating agreement.

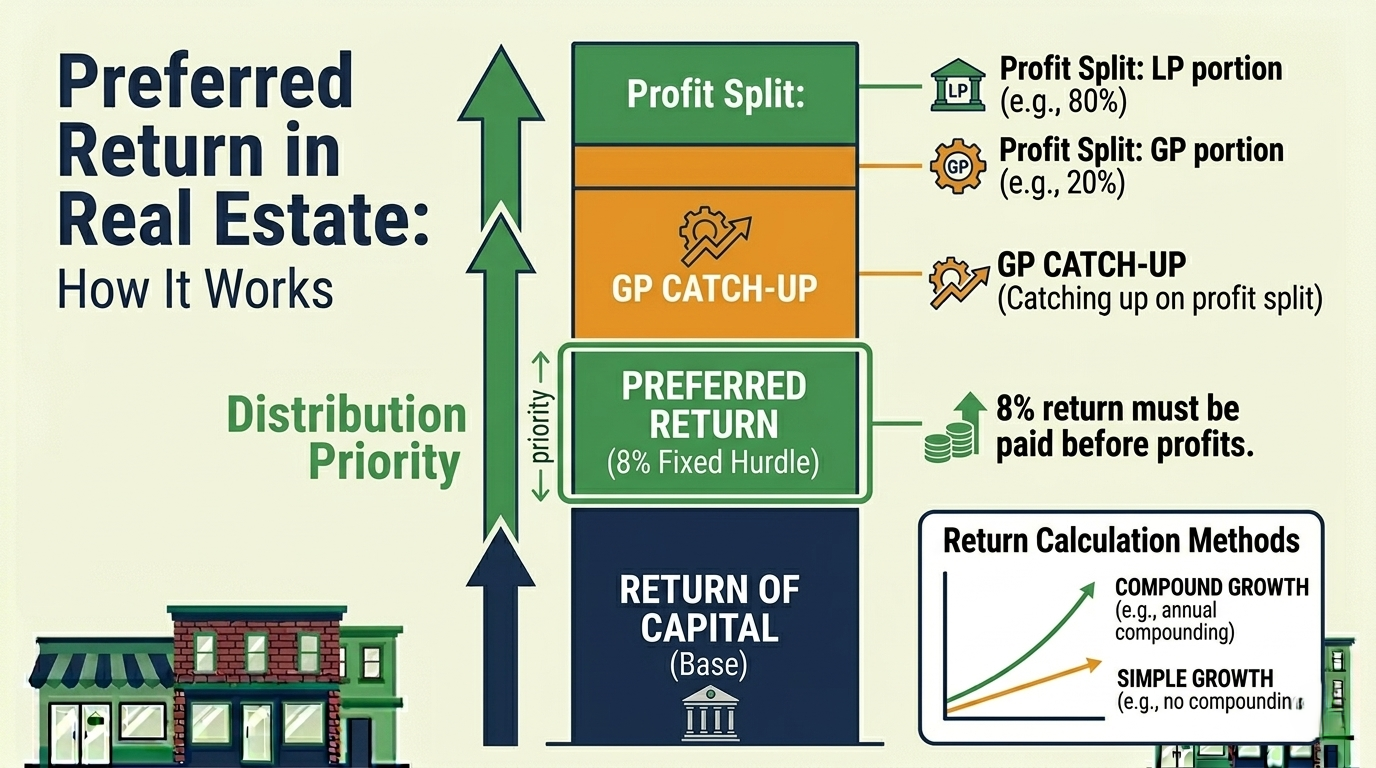

What Is Preferred Return?

Preferred return (or “pref”) is the minimum annualized return that limited partners (LPs) must receive before the general partner (GP) participates in profit sharing.

It’s NOT a guaranteed return. It’s a priority of distribution — LPs get paid first, but only if the deal produces enough cash flow.

Simple example:

An LP invests $100,000 in a deal with an 8% preferred return. Before the GP receives any profit split, the LP must receive $8,000 per year (or its cumulative equivalent).

If the deal only generates $5,000 of distributable cash in Year 1, the LP receives all $5,000 and the remaining $3,000 of unpaid pref accrues — it’s owed but not yet paid.

Simple vs. Compound Preferred Return

This is where most confusion starts. The operating agreement will specify one of two accrual methods, and the difference compounds dramatically over time.

Simple Preferred Return

The pref accrues on the original invested capital only. Unpaid amounts accumulate but don’t generate additional return.

Worked Example — Simple Pref:

LP invests $500,000 at an 8% simple preferred return. The deal pays no distributions for 3 years (common in development or heavy value-add), then distributes $200,000 in Year 4.

| Year | Accrual | Cumulative Owed | Paid | Remaining Owed |

|---|---|---|---|---|

| 1 | $40,000 | $40,000 | $0 | $40,000 |

| 2 | $40,000 | $80,000 | $0 | $80,000 |

| 3 | $40,000 | $120,000 | $0 | $120,000 |

| 4 | $40,000 | $160,000 | $200,000 | $0 (caught up) |

After Year 4, the LP has received $200,000 — which covers the full $160,000 of accrued pref. The remaining $40,000 is the beginning of the GP’s catch-up or the first split above the pref.

Notice: Year 2’s accrual is still $40,000, NOT $40,000 + unpaid from Year 1. That’s simple accrual.

Compound Preferred Return

The pref accrues on the original capital PLUS any unpaid, accrued pref. Unpaid pref earns its own return.

Worked Example — Compound Pref (same scenario):

LP invests $500,000 at an 8% compound preferred return. No distributions for 3 years, $200,000 distributed in Year 4.

| Year | Accrual Basis | Accrual | Cumulative Owed | Paid | Remaining |

|---|---|---|---|---|---|

| 1 | $500,000 | $40,000 | $40,000 | $0 | $40,000 |

| 2 | $540,000 | $43,200 | $83,200 | $0 | $83,200 |

| 3 | $583,200 | $46,656 | $129,856 | $0 | $129,856 |

| 4 | $629,856 | $50,389 | $180,245 | $200,000 | $0 (caught up) |

Under compound accrual, the LP is owed $180,245 through Year 4 — compared to $160,000 under simple accrual. That’s a $20,245 difference on a $500,000 investment over just 4 years.

The gap widens significantly on longer holds or deals where distributions are deferred.

Which Is More Common?

- Institutional deals: Compound accrual is standard. LPs expect their unpaid pref to earn a return.

- Smaller syndications: Simple accrual is more common. GPs prefer it because it limits the compounding effect on their promote.

- Always check the operating agreement. The words “preferred return” mean nothing without specifying the accrual method.

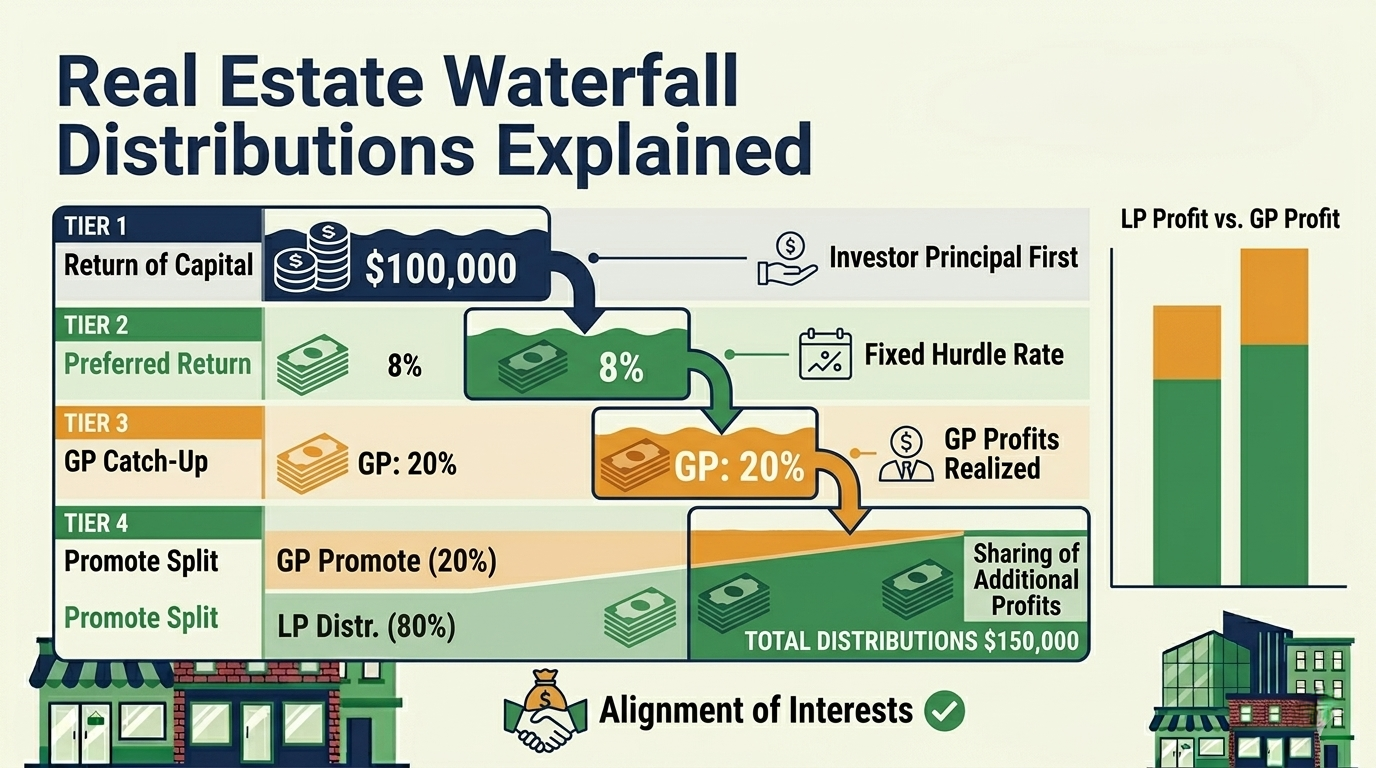

The Catch-Up Provision

After LPs receive their preferred return, many waterfall structures include a catch-up — a period where the GP receives 100% (or a large percentage) of distributions until they’ve “caught up” to a specified share of total profits.

Why it exists: Without a catch-up, the GP doesn’t earn their promote until distributions exceed the pref. The catch-up accelerates GP compensation so they reach their target split faster. For a full walkthrough of how catch-ups fit within multi-tier structures, see our waterfall distributions guide.

Typical catch-up example:

- 8% preferred return to LPs

- 100% catch-up to GP until GP has received 20% of total distributions

- 80/20 LP/GP split thereafter

Worked example:

Deal distributes $100,000 of profit. LP invested $500,000, GP invested $0 (promote only).

Step 1: Preferred Return LP receives first $40,000 (8% × $500,000)

Step 2: GP Catch-Up GP needs to “catch up” to 20% of total distributed. After Step 1, $40,000 has been distributed, all to the LP.

The GP receives 100% of the next distributions until:

GP receives the next $10,000 (because $10,000 / $50,000 total = 20%). Now total distributed = $50,000 (LP: $40K, GP: $10K).

Step 3: Remaining Split (80/20) Remaining $50,000 splits 80/20:

- LP: $40,000

- GP: $10,000

Final Totals:

- LP: $40,000 + $40,000 = $80,000 (80%)

- GP: $10,000 + $10,000 = $20,000 (20%)

The catch-up ensured the GP reached 20% of total distributions, as intended by the promote structure.

Lookback Provisions

A lookback (or “true-up”) provision recalculates the preferred return at the end of the deal using actual cash flows rather than projections.

Why it matters: Deals often distribute inconsistently — heavy cash flow in some years, none in others. A lookback ensures that the LP receives the full preferred return over the ENTIRE hold period, not just on an annual basis.

Example:

An 8% pref with a lookback, $500,000 invested, 5-year hold:

Total pref owed over 5 years (simple): $200,000

If the LP received $220,000 in total distributions during the hold, the lookback confirms they exceeded their pref — the GP’s promote is properly earned.

If the LP received only $180,000, the lookback triggers an additional $20,000 payment to the LP from the GP’s share of exit proceeds.

Clawback Provisions

A clawback is the GP’s counterpart to the lookback. If the GP received promoted distributions during the hold but the deal underperforms at exit, the GP must return excess promote to the LP.

Example: The GP received $50,000 in promotes during years 1-4 based on annual distributions. At exit in Year 5, the LP’s total return falls below the preferred return threshold.

The clawback requires the GP to return up to $50,000 of previously received promote until the LP’s preferred return is fully satisfied.

In practice: Clawbacks are included in most institutional operating agreements but rarely enforced. Many GPs negotiate:

- A clawback cap (e.g., 50% of promote received)

- An escrow requirement (portion of promote held until exit)

- A time limit on the clawback obligation

What to Look for in the Operating Agreement

When reviewing the preferred return section of an OA, check these specific provisions:

1. Accrual method — Simple or compound? This single word changes the math significantly.

2. Accrual frequency — Annual, quarterly, monthly, or daily? Monthly compounding on an 8% annual rate yields more than annual compounding.

3. Cumulative vs. non-cumulative — Cumulative means unpaid pref carries forward. Non-cumulative means if the deal can’t pay the pref in a given year, that year’s pref is forfeited (rare in real estate, common in corporate preferred stock).

4. Return OF capital vs. return ON capital — The pref is a return ON capital. Return OF capital (getting your original investment back) is a separate waterfall tier that typically comes first.

5. Catch-up percentage — Is it 100% to GP or split (e.g., 50/50)? A 100% catch-up benefits the GP; a split catch-up benefits the LP.

6. Lookback and clawback — Are they present? What are the limits? Is there an escrow?

7. Hurdle vs. preferred return — A hurdle is an IRR threshold that gates promoted returns. A pref is a current-return priority. They’re different mechanics that serve similar purposes but produce different outcomes, especially in deals with irregular cash flows.

Common Mistakes

Mistake 1: Confusing pref with guaranteed return. The pref is a priority, not a promise. If the deal loses money, the LP may never receive their pref.

Mistake 2: Ignoring the accrual method. An “8% pref” with compound accrual on a deal with deferred distributions is VERY different from an “8% pref” with simple accrual on a deal with current-pay distributions.

Mistake 3: Not modeling the full waterfall before investing. Run the numbers through every scenario — base case, downside, and upside. See exactly how much the GP earns relative to the LP in each scenario.

Mistake 4: Focusing on pref rate instead of total return. A deal with a 6% pref and a 20% projected IRR may outperform a deal with a 10% pref and a 13% projected IRR. The pref is one component of total return, not the whole picture.

Key Takeaways

-

Preferred return is a priority of distribution, not a guarantee. LPs get paid first, but only from available cash flow.

-

Simple vs. compound accrual creates material differences in dollar payouts. Always verify which method the OA specifies.

-

The catch-up provision determines how quickly the GP participates in profits. Model it explicitly in your waterfall calculations.

-

Lookback and clawback provisions protect against uneven distribution timing. Their presence (or absence) significantly changes the risk profile.

-

Every waterfall term interacts with every other term. You can’t evaluate the pref in isolation — model the full distribution waterfall across multiple scenarios.

Eric Davis is the founder of Nordic Real Estate Services and creator of Solsten, a CRE analysis platform with built-in waterfall distribution modeling, preferred return calculations, and GP/LP return analysis. Model your waterfall →

Try Solsten Free

See everything we discussed in action — no credit card required.

Start Your Free AnalysisRelated Articles

Real Estate Waterfall Distributions Explained: GP/LP Structures for CRE

Complete guide to real estate waterfall distribution structures — how GP/LP splits work, preferred returns, catch-up provisions, promote tiers, and how to model waterfall economics for commercial real estate deals.

How to Build a Real Estate Proforma: Step-by-Step Guide

Learn how to build a commercial real estate proforma from scratch — revenue projections, expense modeling, NOI, debt service, cash flow, and return metrics explained with examples.

Mastering IRR and NPV: How to Assess an Investment's True Profitability

A complete guide to IRR and NPV for real estate investors — formulas, step-by-step examples, MIRR, WACC, sensitivity analysis, and when to trust which metric.