Cap Rates, Do They Really Matter?

When shopping for a new investment property, one of the most common metrics that gets thrown around is the capitalization rate, better known as the cap rate. On its face, a cap rate is a quick and easy way to gauge your expected return and estimated property value when comparing properties against each other.

However, while cap rates are extremely useful as a starting point, relying on them alone can be misleading. There are several critical factors that a cap rate does not capture.

Cap Rates and Debt/Financing

A cap rate is calculated by dividing the net operating income (NOI) by the property’s purchase price or market value. What this equation does not account for is debt — and most investors use financing to purchase property.

The interest rate your bank charges, the loan terms, and the amortization schedule can have a dramatic impact on your actual return. Two properties with the same cap rate can produce very different cash flows depending on how they are financed. A property with a high cap rate may still underperform after debt service if the financing terms are unfavorable.

This is why metrics like cash-on-cash return and levered IRR are essential complements to the cap rate.

Non-Operating Expenses

Cap rates only consider net operating income — the income after operating expenses. What they do not factor in are capital expenditures such as roof replacements, HVAC overhauls, parking lot repaving, or tenant improvements. These expenses can be significant and will directly impact your actual returns.

A property with a great cap rate might come with a laundry list of deferred maintenance that will eat into your profits for years. Always look beyond the cap rate and assess the capital expenditure outlook.

Market Rent Growth

A cap rate is a point-in-time snapshot. It tells you what the return looks like today based on today’s rents, but it tells you nothing about where rents are headed. A property in a high-growth market with moderate current rents may outperform a property in a stagnant market that has a higher cap rate today.

Understanding the local market dynamics — job growth, population trends, supply pipeline — is critical to evaluating whether today’s cap rate will expand or compress over your hold period.

Value-Add Opportunity

Some of the best commercial real estate deals have mediocre cap rates at acquisition because they have below-market rents, deferred maintenance, or management inefficiencies. Savvy investors look for value-add opportunities where they can improve NOI through renovations, better management, or lease-up of vacant space.

In these scenarios, the going-in cap rate is almost irrelevant — what matters is the stabilized cap rate after improvements are complete.

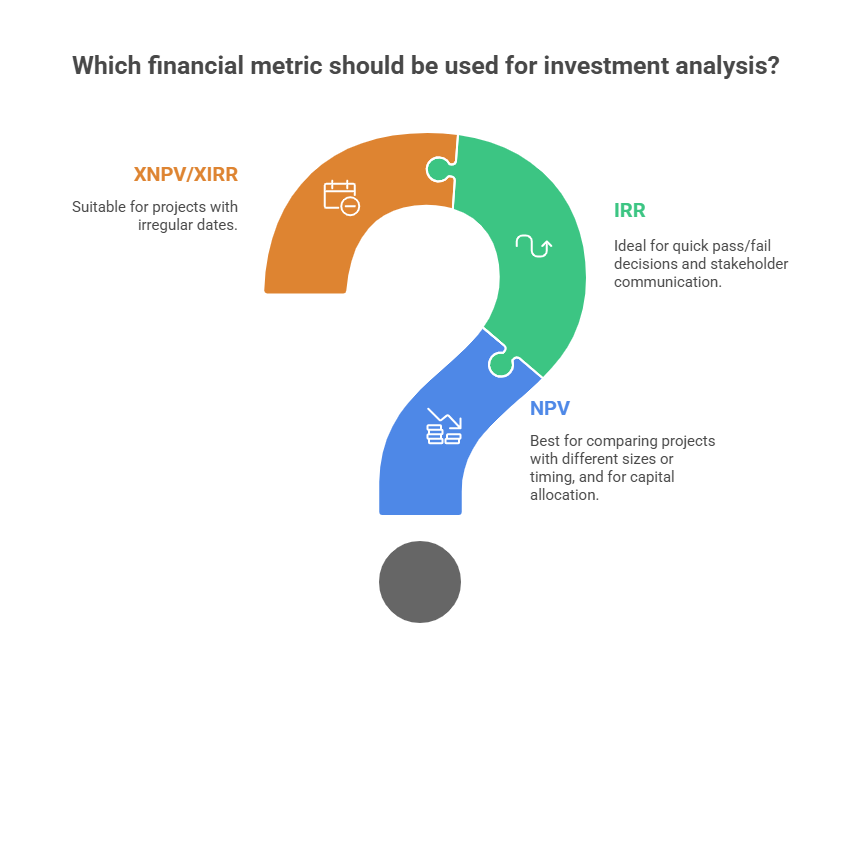

What Metrics Should I Use?

Cap rates are a great starting point for comparing properties, but they should never be your only metric. For a comprehensive analysis, consider:

- Cash-on-Cash Return — tells you the actual cash yield on your equity investment after debt service

- Internal Rate of Return (IRR) — captures the time value of money across the entire hold period, including the sale

- Net Present Value (NPV) — tells you the dollar value created by the investment at your target discount rate

- Debt Service Coverage Ratio (DSCR) — measures whether the property’s income can comfortably cover the mortgage payments

Using these metrics together gives you a much more complete picture than a cap rate alone ever could. Tools like Solsten calculate all of these automatically so you can make informed decisions backed by real analysis, not just a single number.

FAQs

What is a good cap rate for commercial real estate? It depends on asset class, market, and risk profile. Generally, 5–7% for stabilized assets in strong markets and 7–10% for value-add or secondary markets. Always compare to local benchmarks — see our cap rate calculator guide for detailed ranges by property type.

Is a higher cap rate always better? No. A higher cap rate signals higher risk, not necessarily a better deal. A property with a 9% cap rate may have deferred maintenance, weak tenancy, or market headwinds that justify the discount. Always pair cap rate with IRR and NPV for the complete picture.

Why doesn’t cap rate account for financing? Cap rate measures the unlevered yield — the property’s return independent of how it’s financed. This makes it useful for comparing properties on equal footing, but it misses the impact of debt on your actual returns. That’s why cash-on-cash return is the essential complement.

How often do cap rates change? Cap rates shift with interest rates, market supply/demand, and investor sentiment. They can move significantly within a single year during rate-hiking or rate-cutting cycles.

Related Articles

- Best Valuation Tools, Cap Rate Calculators & Strategy Guide — Cap rate tools and value-add vs. core-plus strategy

- Mastering IRR and NPV — The time-value-of-money metrics that complement cap rates

- Free Tools to Calculate Value for Income Properties — NOI calculators and DSCR analysis

Explore Solsten

- 15-Factor Risk Scoring — Go beyond cap rate with DSCR, LTV, WALT, and 12 more factors

- DCF Analysis Software — IRR, NPV, and exit scenario optimization

- CRE Proforma Software — Full operating statements with NOI and cash flow projections

Try Solsten Free

See everything we discussed in action — no credit card required.

Start Your Free AnalysisRelated Articles

What You Need To Know About Cash-On-Cash Return

Learn what cash-on-cash return is, how to calculate it with a step-by-step example, and what a good cash-on-cash return looks like for CRE investments.

Free Tools to Calculate Value for Income-Generating Properties

A practical guide to using free valuation platforms, NOI calculators, and cap rate formulas to analyze income-producing real estate — featuring Solsten as a top free-tier platform.

What Does A Good IRR Look Like?

Learn what internal rate of return (IRR) means for commercial real estate, the difference between levered and unlevered IRR, and what ranges smart investors target.