What Is Cash-On-Cash Return? Formula, Example, and Benchmark

What Is Cash-On-Cash Return?

Cash-on-cash return on investment (cash-on-cash ROI) is one of the most important real estate investing metrics you need to know. Cash-on-cash return is the cash flow in your pocket as a percentage of the equity invested in the deal. Essentially, it measures what percentage of the money you put into a deal you get back each year.

It’s a simple calculation, but finding the variables to calculate it can be a little complex.

How to Calculate Cash-On-Cash Return

For simplicity, we will assume that we have all the primary data points readily available. In real life, you will have to contact your bank to get an estimate on the interest rate they would charge, loan terms, amortization schedule, and closing costs. When it comes to capital expenses, this may require a contractor to give you estimates. You also may have to consider leasing commissions paid to a broker finding you a new tenant.

The Setup

For this example:

- Purchase price: $3,750,000

- Closing costs: $100,000

- Down payment: 25%

- Interest rate: 4.75%

- Amortization: 30 years

- Year 1 NOI: $275,000

- Year 1 capital expenses: $10,000

Step 1: Calculate the Loan Amount

Step 2: Calculate Your Equity Invested

Step 3: Calculate Annual Debt Service

Using the PMT function:

Step 4: Calculate Cash Flow After Debt Service

Step 5: Calculate Cash-On-Cash Return

This means in the first year you will receive 8.57% back out of the equity you invested.

Generally speaking, cash-on-cash return is your income for that year minus all expenses, divided by the equity invested. This tells you that out of the money you invested, you have received that percentage back for that fiscal year.

What Is a Good Cash-On-Cash Return?

Now that we understand how to calculate it, what is a good cash-on-cash return? Like internal rate of return, there are a few factors to consider.

Risk Level

The higher the risk of the investment, the higher the returns you should expect. The lower the risk, the lower the returns you should expect.

What Cash-On-Cash Doesn’t Capture

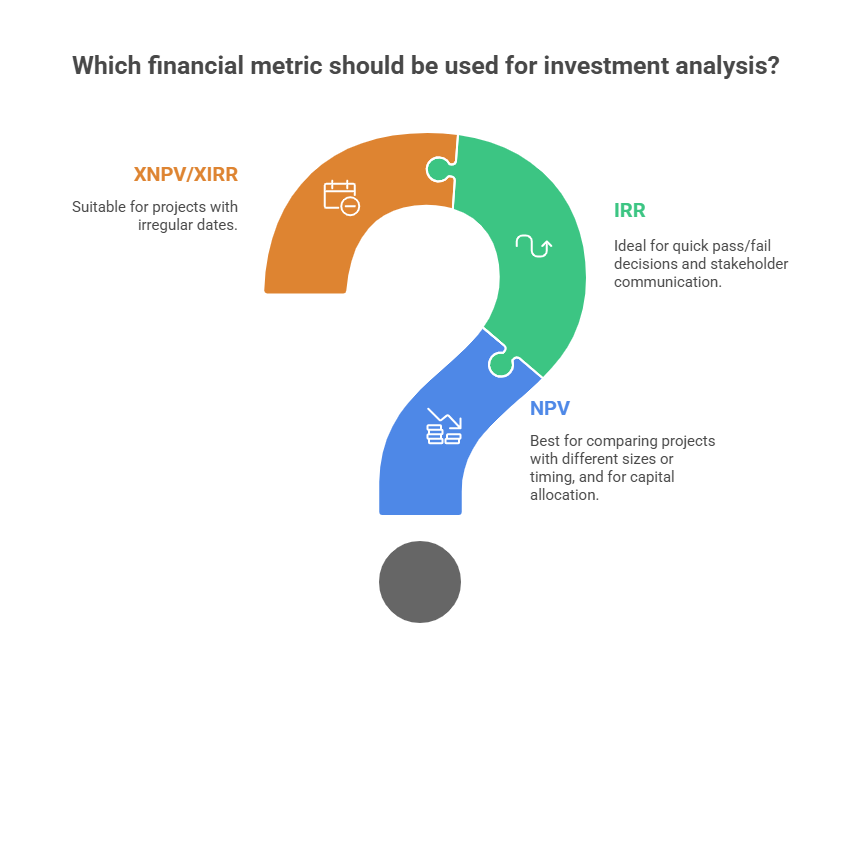

Cash-on-cash return does not consider tax benefits — for example, depreciation write-offs or the appreciation of your property’s value through time. That is why it is crucial to cross-examine your cash-on-cash return with the IRR, net present value, and debt coverage ratio to make sure you are making a wise investment.

The 8% Rule of Thumb

As a general rule of thumb, if the property is a low-risk investment, you may be comfortable with a cash-on-cash return of around 8%. As the risk rises, so does the return you should expect.

Why 8%? Because if you were to put the equity into the stock market, you could expect an average return of about 9% a year. With stocks, you must pay capital gains taxes every time you sell and reinvest.

Real estate is different — you can write off expenses, interest payments, and depreciation, which cash-on-cash return does not consider. Once these are taken into account, there is a good possibility that you will surpass the stock market’s average return, especially for low-risk properties.

Additionally, when you sell a property, you can do a 1031 exchange — shifting the proceeds to a like-kind property and avoiding capital gains tax. The higher the risk of the investment, the higher the returns you should aim for.

Skip the Manual Math

You don’t need to run PMT formulas or build spreadsheets from scratch. Solsten calculates cash-on-cash return automatically alongside IRR, NPV, DSCR, and a full proforma — all for free. Enter your deal details and get institutional-grade analysis in minutes.

FAQs

What is a good cash-on-cash return for rental property? For low-risk stabilized properties, 8% is a common benchmark. Higher-risk value-add deals should target 10–15%+. The right target depends on your risk tolerance and the opportunity cost of your capital.

How is cash-on-cash return different from cap rate? Cash-on-cash return measures your actual cash yield after debt service relative to your equity investment. Cap rate measures the property’s unlevered yield regardless of financing. Cash-on-cash captures the impact of leverage; cap rate doesn’t.

Does cash-on-cash return account for appreciation? No. Cash-on-cash only measures annual cash flow against equity invested. It doesn’t capture property appreciation, depreciation tax benefits, or the proceeds from a future sale. Use IRR to capture the full return picture including appreciation and exit value.

Can cash-on-cash return be negative? Yes — if your annual cash flow after debt service is negative (the property costs more to operate than it earns), cash-on-cash will be negative. This is common during lease-up or heavy renovation periods in value-add deals.

Related Articles

- CRE Loan Types Explained — The debt structures that determine your cash flow- Cap Rates: Do They Really Matter? — Why cap rate alone isn’t enough

- Mastering IRR and NPV — Time-value-of-money metrics for the complete picture

- What Does a Good IRR Look Like? — Levered vs. unlevered IRR ranges

Explore Solsten

- CRE Proforma Software — Automatically calculate cash-on-cash, IRR, NOI, and more

- DCF Analysis Software — Multi-year projections with exit scenario analysis

- Plans & Pricing — Start your analysis for free

Try Solsten Free

See everything we discussed in action — no credit card required.

Start Your Free AnalysisRelated Articles

What Does A Good IRR Look Like?

Learn what internal rate of return (IRR) means for commercial real estate, the difference between levered and unlevered IRR, and what ranges smart investors target.

Cap Rates, Do They Really Matter?

Cap rates are the most used metric in CRE — but relying on them alone is dangerous. Learn what cap rates miss and which metrics give you the full picture.

Property Manager: Tips Landlords Should Know When Hiring

A comprehensive guide to finding, evaluating, and hiring a property manager — 9 traits to look for, interview questions to ask, and red flags to watch for.