See Where the Deal Breaks Before You Write the Loan

Solsten is DSCR-first CRE loan underwriting software for community banks, private lenders, credit unions, and debt funds. Size deals correctly, stress test downside, flag refinance risk, and track covenants without rebuilding your model for every scenario.

The problem with the tools most lenders reach for

Excel underwriting drifts between deals. Every underwriter has their own template, DSCR calculations diverge, and downside scenarios end up in linked workbooks nobody remembers how to open. When credit committee asks for stress test detail, everyone scrambles.

LOS platforms are workflow, not underwriting. nCino, Encompass, LaserPro, and Baker Hill manage pipeline and approvals. They do not do the loan-sizing math. That still lives in a spreadsheet.

ARGUS Enterprise is priced for institutional CRE debt teams. For a community bank, a private lender, or a credit union commercial team, ARGUS is off-budget and overkill.

Solsten is a third option. Institutional-grade loan underwriting math, transparent methodology, defensible documentation, priced for the lenders who actually need it.

Built for how lenders actually work

- Community bank commercial lending officers running local CRE loans in the $1M to $25M range.

- Regional bank CRE credit analysts underwriting mid-market deals for portfolio and syndication.

- Private lenders, debt funds, and bridge lenders deploying non-bank capital at higher yield.

- Credit unions with commercial lending programs that need institutional documentation without institutional software cost.

DSCR-first modeling

DSCR trajectory over the hold period, covenant tracking, and minimum coverage flags. When DSCR breaks, you see it in the year it breaks, not after the fact.

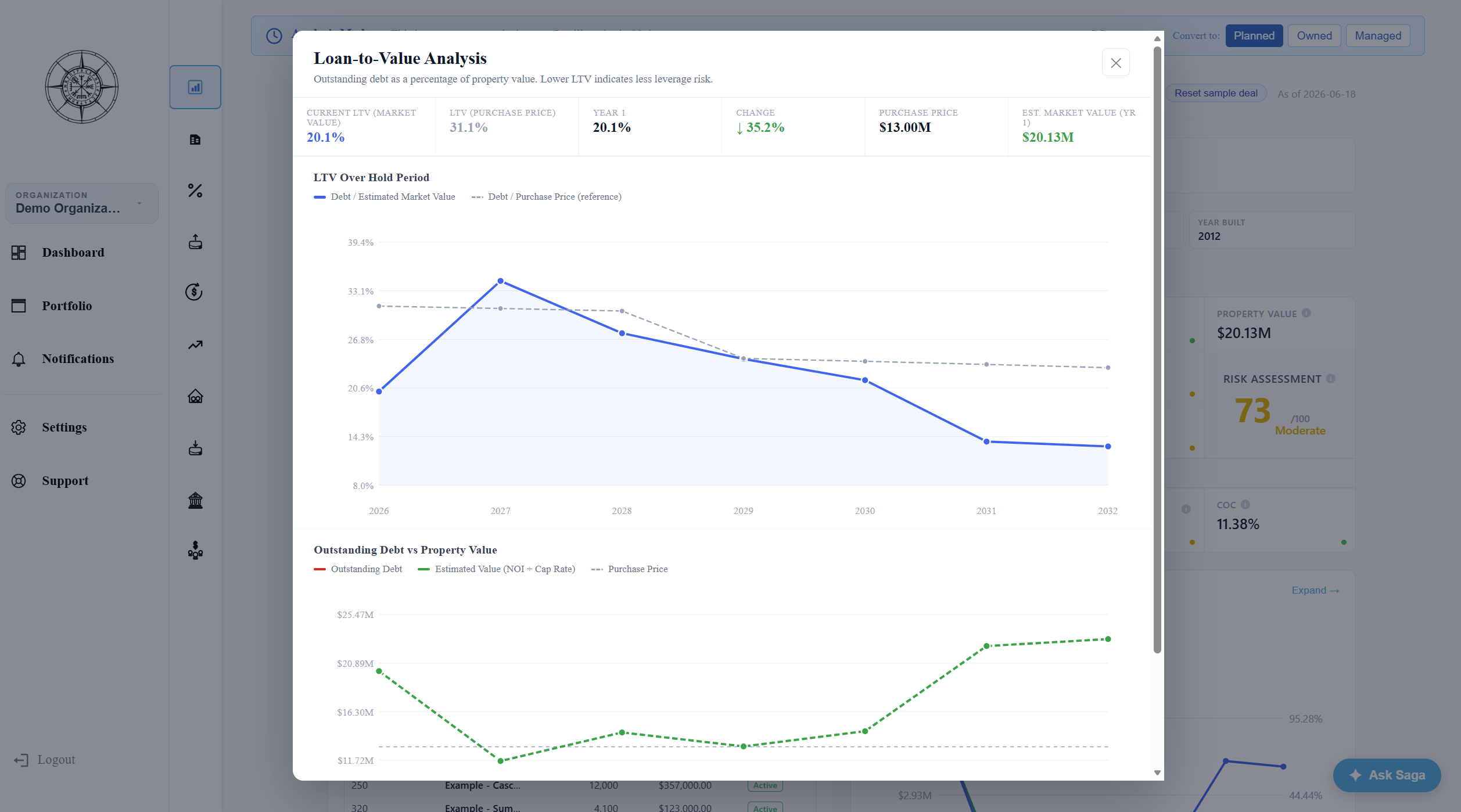

LTV and debt yield

Both metrics side by side, updated in real time as inputs change. LTV at maturity flagged so refinance risk is not a surprise at year five.

Downside stress testing

Vacancy sensitivity, rent decline scenarios, expense inflation shocks, and cap rate expansion. Every assumption documented for credit committee review.

Loan structures that flex

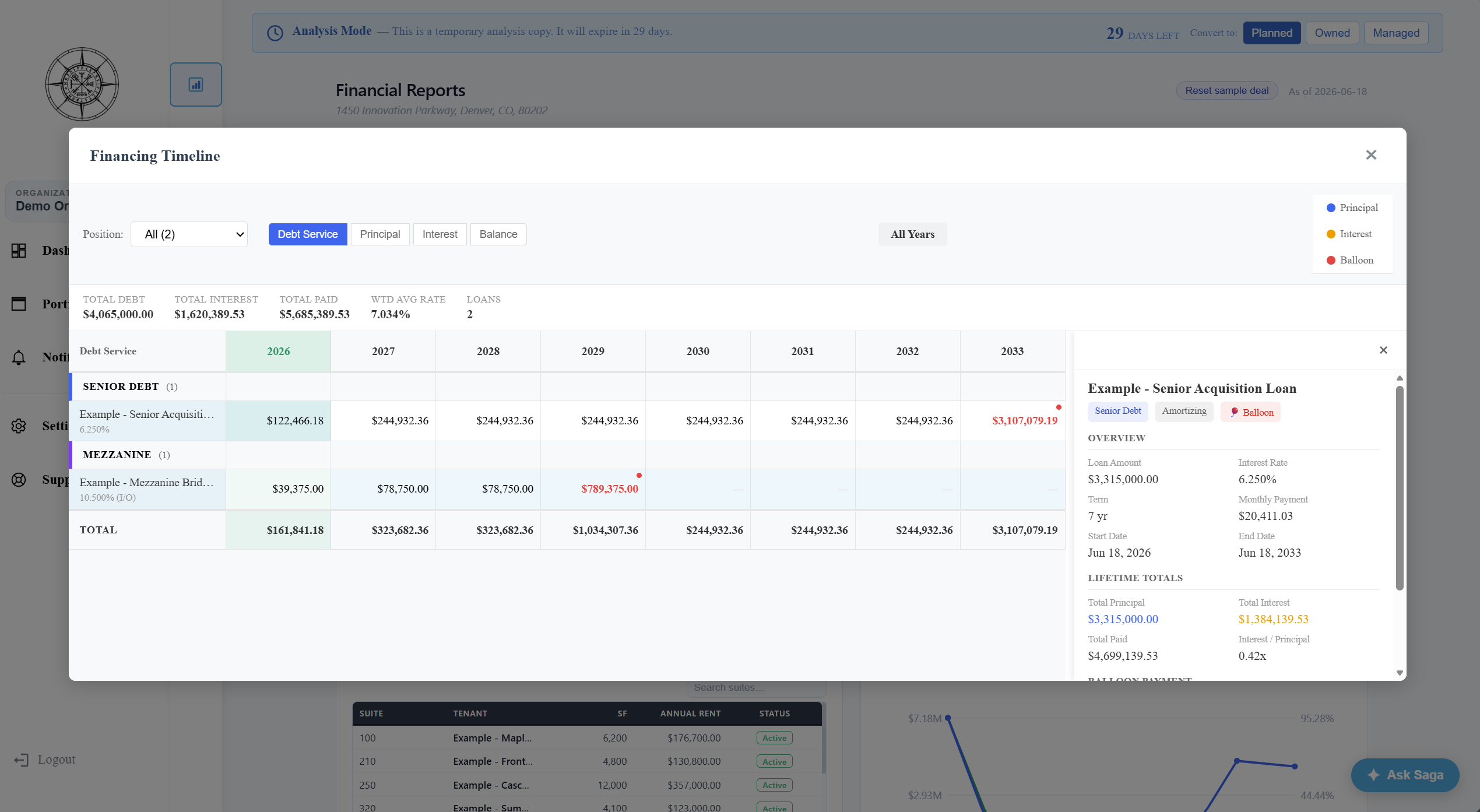

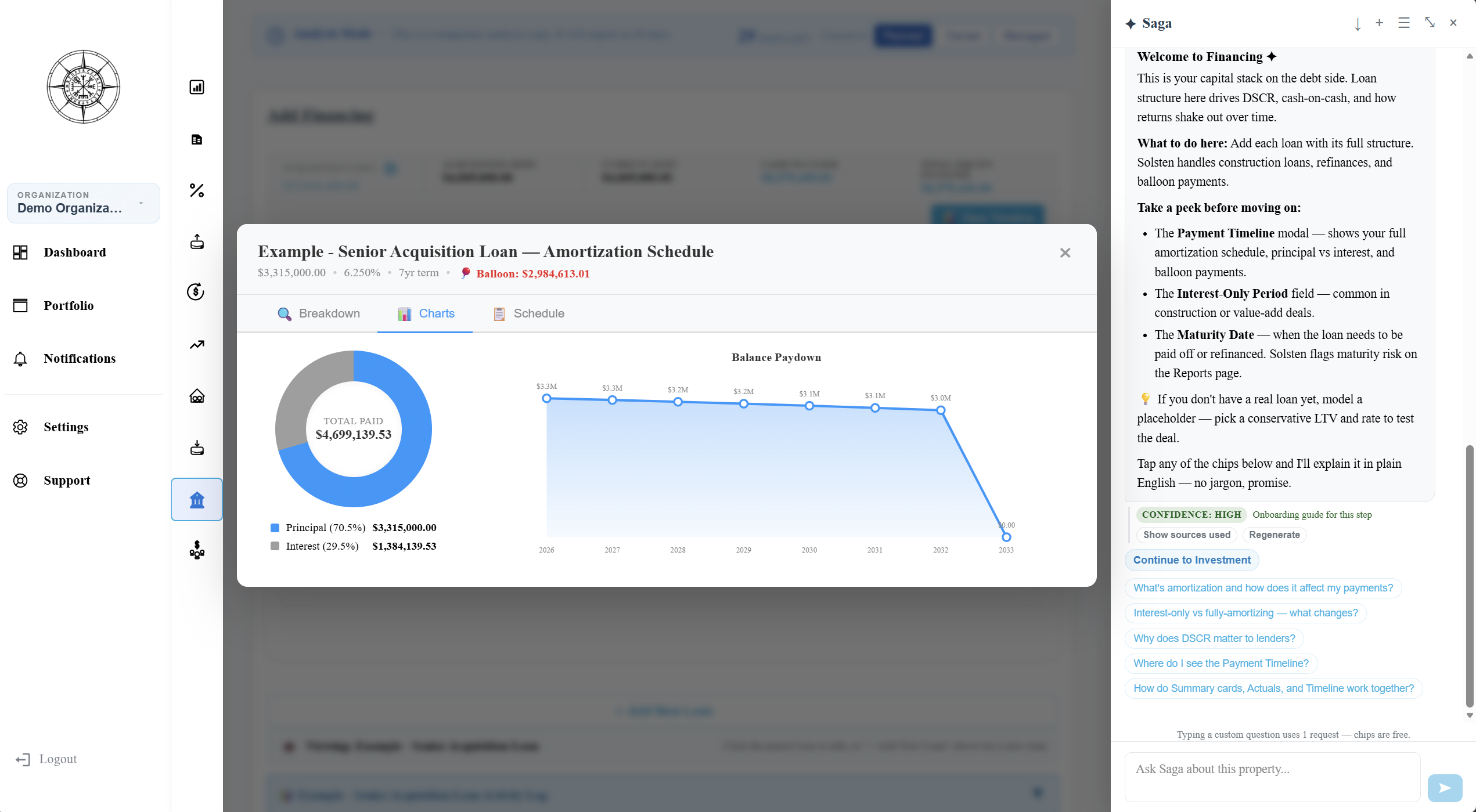

25+ loan fields covering fixed, floating with rate caps, hybrid, construction with draw schedules, bridge, and mezzanine layered on top of senior debt.

See the full life of every loan on the deal

Amortization, DSCR trajectory, LTV progression, refinance events, and balloon maturities plotted year by year across the hold period. When a deal has a refi in year five, you see the takeout math AND what happens if the refinance prices tight or the debt yield does not clear.

Layer multiple loans (senior plus mezz, construction plus perm, bridge plus takeout) and see how they interact. No parallel workbooks. No manual reconciliation. One connected model.

Loan-level detail with a paper trail

Every payment, principal reduction, and interest allocation is documented and traceable. Prepayment penalty math handled. DSCR by period. Behavior under floating rates or hybrid structures visible without a separate calculation.

Auditors, regulators, and credit committee members can read the model without asking a junior analyst to explain what any cell means.

What Solsten is not

Being honest matters more than marketing. Solsten is not a loan origination system, not a credit decisioning platform, and not a loan servicing tool.

Solsten will not replace nCino, Encompass, LaserPro, or Baker Hill for pipeline and workflow. It does not automate approve or decline decisions. It does not handle payment processing, escrow accounting, or regulatory reporting to your call reports.

Solsten is the underwriting math layer that sits alongside your LOS and servicing stack. It replaces the Excel model that lives inside your credit memo, and it does that with the transparency and documentation that credit committee and regulatory review actually require.

FAQs for lenders

Does Solsten replace our loan origination system?

No. Solsten replaces the Excel underwriting model that lives inside the credit memo. Your existing LOS (nCino, Encompass, LaserPro, Baker Hill, or your own workflow tool) still handles the pipeline, approvals, and document generation. Solsten is the underwriting math layer that sits alongside it.

Can Solsten handle construction and bridge loan structures?

Yes. Solsten supports construction loans with draw schedules and takeout structures, bridge loans with balloon flags, floating rate loans with caps and floors, hybrid structures with step-ups, and mezzanine layered on top of senior debt. All 25+ loan fields are visible and editable.

How does Solsten handle refinance and balloon risk?

The financing timeline flags every balloon and maturity event on the loan schedule. You can model the takeout scenario alongside the original loan and see how the deal behaves if the refinance is priced tight, if the debt yield does not clear, or if the takeout gets pushed. Nothing about the risk is hidden in a spreadsheet.

Can we run downside stress tests for credit committee or regulatory review?

Yes. Vacancy sensitivity, rent decline, expense inflation shocks, and cap rate expansion can all be modeled with documented assumptions. Every input is labeled and traceable, which matters when the regulator or an auditor asks how a scenario was constructed.

What can we export as credit memo backup?

Solsten produces three PDF exports: a full Offering Memorandum, a Joint Venture packet, and an Investor packet. The OM export is the closest fit for credit memo backup because it includes the underwriting assumptions and calculation output side by side. Attach it as workpaper or reference material.

See the math for yourself

Methodology Transparency

Read exactly how Solsten calculates NOI, DSCR, IRR, exit value, and every intermediate number that lands in your credit memo.

ARGUS Comparison

Side-by-side feature comparison for CRE debt teams evaluating what they gain and lose moving off ARGUS Enterprise.

Sample Underwrite

A full underwriting packet built entirely in Solsten. See what a borrower or broker would send you and how the math is structured.