Real Estate DCF Analysis Made Simple

Compass automates discounted cash flow analysis for commercial real estate. Get IRR, NPV, equity multiples, and terminal value calculations — with ML-powered forecasting that learns from your property data.

What Is DCF Analysis in Real Estate?

Discounted Cash Flow (DCF) analysis calculates the present value of a property by projecting all future cash flows and discounting them back at an appropriate rate of return.

It answers the fundamental question: "What is this property worth today, given everything I expect it to earn?"

Unlike simple cap rate analysis, DCF accounts for the time value of money, varying cash flows, lease rollovers, rent escalations, vacancy periods, and the terminal sale — giving you a far more accurate picture of investment value.

The DCF Formula

- CFₜ = Cash flow in year t (NOI minus debt service)

- r = Discount rate (your required rate of return)

- n = Hold period in years

- Terminal Value = Sale price at exit (NOI ÷ terminal cap rate)

Compass computes all of this automatically from your property data.

Return Metrics Compass Calculates

Every metric institutional investors and lenders expect to see.

Internal Rate of Return

The annualized return that makes NPV = 0. Compass calculates both leveraged and unleveraged IRR, with Going-Forward and Since Acquisition variants.

Net Present Value

The difference between present value of cash flows and your initial investment. Positive NPV = the deal exceeds your required return.

Equity Multiple

Total distributions divided by total equity invested. A 2.0× equity multiple means you doubled your money.

Cash-on-Cash Return

Annual pre-tax cash flow divided by total cash invested. The real-world yield on your out-of-pocket investment.

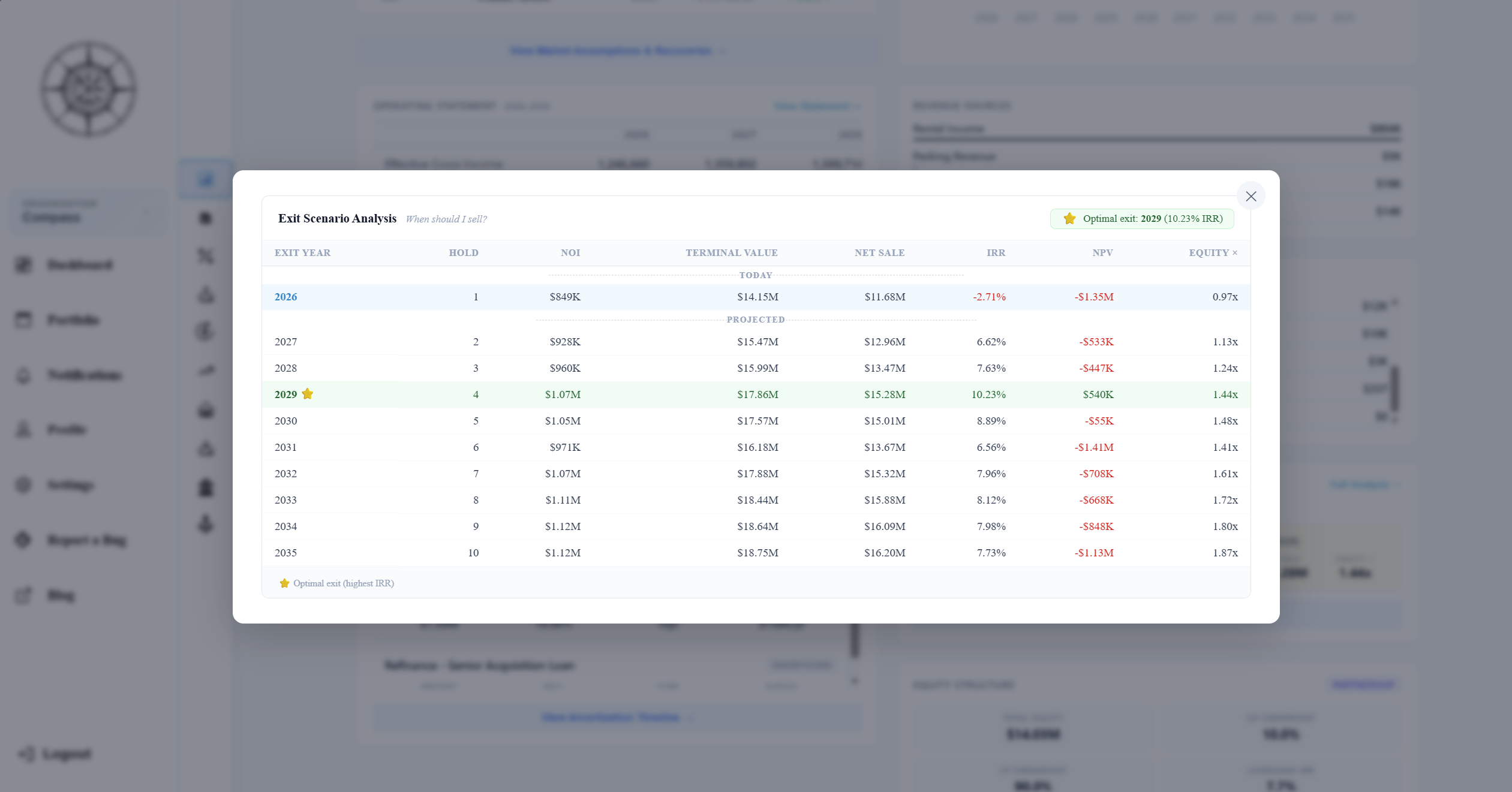

Exit Scenario Optimization

Compass doesn't just calculate returns for your target hold period — it computes IRR, NPV, and equity multiple for every possible exit year.

The Exit Scenario Table highlights your optimal exit year with a star icon, flags loan maturity dates, and shows historical vs. projected periods.

This helps you answer: "Should I hold another year, or sell now?"

Why Compass for DCF Analysis

ML-Calibrated Assumptions

Expense growth rates and rent projections are calibrated from your actual payment history — not just static percentages.

Dual-Metric Returns

Going-Forward returns (from today) and Since Acquisition returns (from purchase date) — with automatic lease coverage gating.

Period-Average Occupancy

ARGUS-standard weighted-average occupancy over billing periods, not point-in-time snapshots. Captures mid-month lease events accurately.

Frequently Asked Questions About DCF Analysis

What is DCF analysis in commercial real estate?

Discounted Cash Flow (DCF) analysis calculates the present value of a commercial property by projecting all future cash flows (rental income minus expenses minus debt service) over a defined hold period, then discounting them back at the investor's required rate of return. It accounts for time value of money, varying cash flows, lease rollovers, vacancy, and the terminal sale value.

What is IRR in real estate?

Internal Rate of Return (IRR) is the annualized rate of return that makes the Net Present Value (NPV) of all cash flows equal to zero. It accounts for the timing and magnitude of every cash flow — including initial investment, operating cash flows, and sale proceeds. A higher IRR means a better risk-adjusted return. Compass calculates both leveraged IRR (after debt) and unleveraged IRR (before debt).

What is a good IRR for commercial real estate?

Target IRRs vary by property type and risk profile. Core stabilized assets typically target 6-10% IRR, value-add investments target 12-18%, and opportunistic deals target 18%+. Leveraged IRR is typically higher than unleveraged due to the magnifying effect of debt. The "right" IRR depends on the investor's return requirements and the risk of the specific deal.

How is terminal value calculated in real estate DCF?

Terminal value (also called reversion value) is the projected sale price at the end of the hold period. It is typically calculated as: Terminal Year NOI ÷ Terminal Cap Rate. For example, if Year 10 NOI is $500,000 and the terminal cap rate is 7%, the terminal value is $7,142,857. This is then discounted back to present value as part of the DCF.

What discount rate should I use for real estate DCF?

Discount rates for commercial real estate typically range from 7-12%, depending on property type, location, tenant quality, and market conditions. The discount rate represents your minimum acceptable return — it should reflect the risk of the specific investment. Core Class A office in a gateway market might use 7-8%, while a value-add retail property might use 10-12%.

What is the difference between NPV and IRR?

NPV (Net Present Value) tells you in dollar terms how much value a deal creates above your required return. A positive NPV means the deal exceeds your hurdle rate. IRR tells you the actual percentage return the deal delivers. Both are essential — NPV helps with go/no-go decisions, while IRR helps compare deals of different sizes. Compass calculates both automatically.

Can Compass replace Excel for DCF analysis?

Yes. Compass generates complete DCF analyses automatically from your property data — including IRR, NPV, equity multiples, exit scenario optimization, and dual-metric returns (Going-Forward and Since Acquisition). Unlike Excel, Compass auto-adjusts projections as time passes, uses ML-calibrated expense forecasts, and eliminates formula errors.

Run Your First DCF Analysis Free

Enter your property data and get IRR, NPV, equity multiple, exit scenarios, and a complete operating statement — automatically.

No credit card required. Full access during beta.